S&P500 Trading Update 8/4/26

S&P500 Trading Update 8/4/26

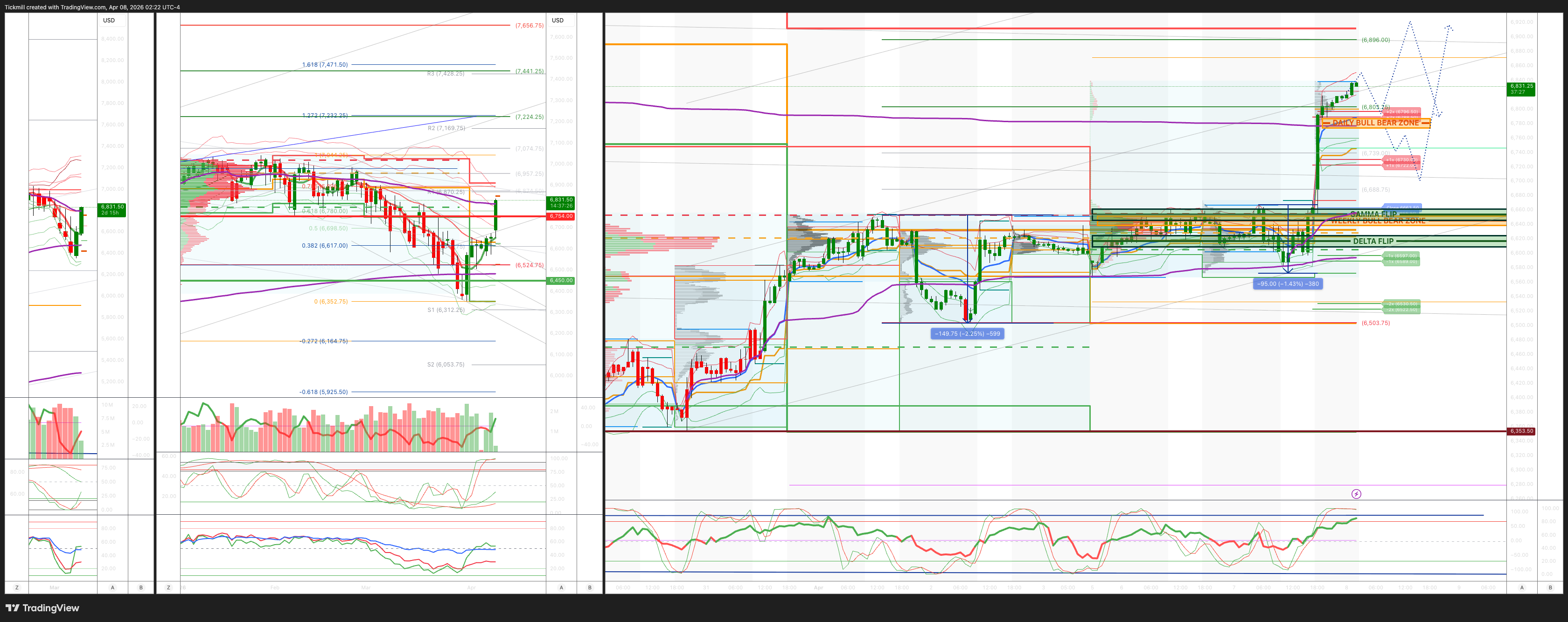

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6640/50

WEEKLY RANGE RES 6754 SUP 6450

April OPEX Straddle: 328.55pt range implies a OPEX to OPEX range of [6177, 6835]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

PUT/CALL RATIO 1.26 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 6654

WEEKLY VWAP BULLISH 6591

MONTHLY VWAP BULLISH 6816

DAILY STRUCTURE – OTFH - 6598

WEEKLY STRUCTURE – BALANCE

MONTHLY STRUCTURE - OTFD - 6911

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6570/60

GAMMA FLIP 6653

DAILY RANGE RES 6731 SUP 6584

2 SIGMA RES 6796 SUP 6588

VIX BULL BEAR ZONE 22

TRADES & TARGETS

LONG ON REJECT/RECLAIM OF DAILY BULL BEAR ZONE TARGET 6910/20

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Pre Ceasefire’

The S&P 500 wrapped up the day with an uptick of 8 basis points, closing at 6,617, buoyed by a market-on-close (MOC) buy of $1.8 billion. The Nasdaq Composite also saw a slight rise of 4 basis points, settling at 24,202, while the Russell 2000 gained 21 basis points to reach 2,545. In contrast, the Dow Jones Industrial Average dipped by 18 basis points to end at 46,584. Overall, trading activity was relatively subdued, with 18.83 billion shares exchanged across U.S. equity markets, slightly below the year-to-date daily average of 19.5 billion shares.

The volatility index (VIX) surged by 675 basis points to hit 25.83, while WTI crude oil prices fell by 6 basis points to $112.34. The yield on the U.S. 10-year Treasury note decreased by 3 basis points to 4.30%. Gold prices rose by 123 basis points to $4,708, the dollar index (DXY) dropped by 32 basis points to 99.66, and Bitcoin saw a decline of 58 basis points to $69,428. Notably, the S&P has now recorded five consecutive sessions of gains, a streak not seen since October.

Trading was quiet today, with volumes down by 22% compared to the 20-day average as investors adopted a 'wait and see' approach ahead of President Trump’s 8 PM deadline for Iran to agree to a ceasefire. Late in the day, news from Pakistan's Prime Minister Sharif indicated that diplomatic efforts were progressing, with a request for Trump to extend the deadline by two weeks and for Iran to open the Strait of Hormuz as a goodwill gesture.

Our trading floor activity was rated a mere 3 on a scale of 1-10 in terms of overall engagement, finishing with a net sale of -807 basis points compared to a 30-day average of -114 basis points. Single-stock trading remained muted, with asset managers and hedge funds collectively selling around $1 billion, primarily in macro, discretionary, and energy sectors.

Key highlights included:

1. AVGO saw a gain of 2% after announcing a long-term partnership with GOOGL to develop and supply Tensor Processing Units (TPUs).

2. AAPL faced a decline of 2%, testing its 200-day moving average amidst concerns raised by a Nikkei article regarding issues with foldable iPhone engineering.

3. Managed care stocks rose by 4% following the release of Medicare Advantage rates showing a +2.48% increase—significantly above the ~1% target.

Despite clarity on Medicare Advantage rates, our healthcare flows were erratic, indicating a lack of consensus among investors. Earnings season kicks off tomorrow with Delta Airlines (DAL) reporting. The stock is expected to move by 6%, having performed positively in four out of the last five quarters. The current Q1 earnings per share (EPS) guidance is between $0.50 and $0.90, with full-year estimates at $6.50 to $7.50, compared to consensus figures for Q1 and 2026 at $0.58 and $5.94, respectively.

DAL recently raised its revenue guidance in mid-March, which is noteworthy given the ongoing conflict in the Middle East, now projecting high single-digit revenue growth for Q1 compared to previous expectations of +5-7%. The focus now shifts to Q2 estimates (consensus at $1.81, down from $2.60) and full-year projections (Street at $5.94, down from $7.20), with buy-side estimates leaning closer to $1.50 and $5.50 respectively.

In derivatives, attention remains on the ongoing negotiations with Iran and Trump’s impending deadline, causing stress in the volatility market. The VIX spiked over three points by mid-afternoon, while UX1 reached highs later in the session, significantly outperforming its beta relative to the S&P. Heading into tomorrow's close, an implied move of approximately 1.5% is anticipated. Flows showed buying interest in both call and put options, particularly in shorter-dated contracts. The SPX straddle increased from an initial 1.95% this morning to 2.25%.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!